Articles

Part 2: Will Automated Market Makers (AMMs) disrupt the traditional order book model?

Introduction In part one, we explored the market-making landscape and began to unpack how Automated Market Makers (AMMs) function. In part two, we will examine in greater detail the benefits…

Introduction

In part one, we explored the market-making landscape and began to unpack how Automated Market Makers (AMMs) function. In part two, we will examine in greater detail the benefits and drawbacks of trading with AMMs, as well as how a favorable regulatory environment could present an unprecedented opportunity for banks to enter the space.

What are the pros and cons of AMMs?

AMMs function by being built on blockchains, using the technology to enable and track deposits into the liquidity pools, facilitate the transfer of assets and minimize trust required between counterparties. This comes with a number of inherent positives and negatives which are worth keeping in mind.

Pros

The key benefit to using an AMM, apart from the broadening of market participants able to engage in market making, is optimized liquidity. By definition, order books only have liquidity at a narrow range around the converged upon market price, causing slippage if large orders are placed. Modern AMMs use something called concentrated liquidity, in which they concentrate the liquidity in a pool around a price range of an asset, causing liquidity at common price levels to be deeper, and capital up to 40 times more efficient. This increased capital efficiency not only paves the way for low slippage trading which can surpass most CLOB models, but also helps banks to optimize collateral and meet regulatory requirements. Additionally, even smaller trades can experience slippage in traditional order book systems if there are not enough limit orders to fill a trade, whereas small trades are highly unlikely to experience noticeable slippage in an AMM as the pool provides immediate liquidity at the market price.

Cons

There are two key forms of drawbacks to AMM adoption; implementation risk and systemic limitations. The critical risk for firms looking to enter the AMM space, is the cost and risk of replacing legacy systems which have been designed to feed into CLOB-based structures. Front-office transformation is historically expensive and time-consuming, so implementing the infrastructure necessary to enable AMMs would carry significant investment risk.

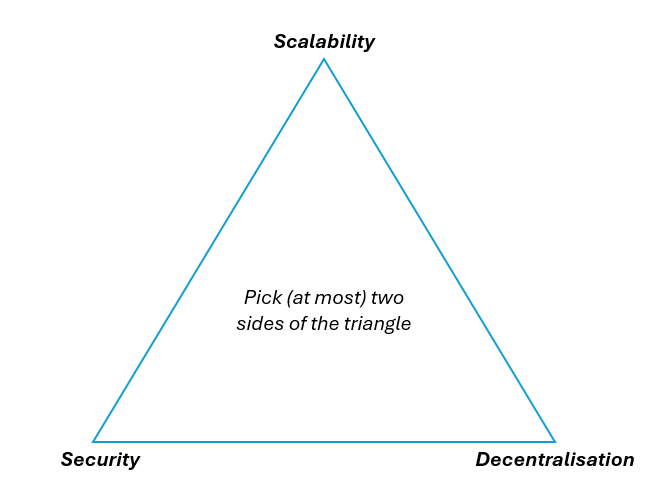

The most immediate systemic limitation for AMMs transacting on top of the blockchain is latency. To be able to meet the demands of the modern market participants, any system used for trading must be able to handle hundreds of millions of transactions at any given moment. Traditionally, blockchains have been plagued by slow transaction time due to the complex computing operations which have to happen in the background. In DeFi, this is thought of as the scalability trillema, a common blockchain thought experiment, in which anything built on-chain must choose only two of security, scalability (read, speed) and decentralisation, and pick which attribute to trade off. However, if banks choose to enter this space, we can assume the blockchain being built on is proprietary and centralized, meaning we implicitly choose to trade off decentralisation for scalability. Hence, a bank or financial institution building an AMM on a centralized blockchain may go some way to solving this scalability issue. Indeed, driving enough scalability would also go some way to mitigating the investment risk discussed above, as the AMM may be able to generate enough revenue to provide significant ROI.

In summary, DeFi and AMMs have removed the need for a centralized counterparty in executing and pricing trades, offering an opportunity for markets to move towards laissez-faire economic ideals. Rather than relying on intermediaries and market makers, the market systemically makes a market at a price which suits all market participants. Despite this, some of the fundamental downsides of transacting on the blockchain as well as implementation risks, provide some challenges for large-scale financial market infrastructure adoption.

How is the landscape shifting?

In truth, seeing AMMs become the prevalent method of exchange would require a fundamental shift within financial market infrastructure, supported by a favorable regulatory environment. However, this does not preclude AMMs from baring a significant first-mover advantage for traditional finance institutions.

The Trump presidency has signaled a large regulatory shift deemed favorable for digital asset classes. Whereas the outgoing SEC Chair Gary Gensler was critical of digital assets, Trump’s nominee Paul Atkins is already looking at a policy of deregulation. While many may focus on the trading of digital assets themselves due to their volatility and eye-catching charts, delivering a trustworthy, reliable and reputable platform for trading these assets may be undervalued. Therefore, there could be an opportunity for firms to explore how to efficiently provide digital asset markets to both institutional and retail clients using AMMs.

What should firms be thinking about?

Whilst the order book is unlikely to disappear any time soon, firms should continue to be pragmatic in assessing the uses of emerging technologies. We have seen a number of firms successfully adopt digital asset technology for various use-cases, including J.P Morgan’s Kinexys blockchain which has serviced upwards of $2 trillion in transaction volume, HSBC’s FX Everywhere which has settled $2.5 trillion in FX volume since 2018, Goldman’s Digital Assets Platform which issued the first on-chain bond in 2023, and Citi’s Integrated Digital Assets Platform which offers centralized token issuance.

We can see that the digital asset space is once which banks are keen to play in, but none have yet taken the opportunity to leverage AMMs to provide a digitally-native method of exchange, and realize the benefits we have discussed here. Whilst traditionally fully decentralised, in theory a semi-centralized system could exist in which firms facilitate an AMM, collecting trading fees and paying a proportion to liquidity providers. This allows firms to benefit from the increased efficiency of AMMs whilst mitigating their usual regulatory risk and scalability issues. This centralisation of technology previously considered decentralised has been proven, as in the case of Kinexys, attracting customers with increased trust and regulatory efficacy.

In summary, whilst the CLOB will not cease to exist in the near term, the success of trading infrastructure in DeFi means that change is likely coming, especially in digital asset classes. We know that both trader behavior and regulators’ priorities cannot always be predicted, and so it is key that banks look at how adopting a hybrid model could be accretive to their bottom lines. CLOBs can continue to provide larger trading volumes in traditional liquid markets and access to legacy data, whilst AMMs can increase price stability and provide quicker access to digital asset markets and liquidity. This hybrid approach allows banks to capitalize on a lucrative and competitively advantageous space of AMMs, whilst retaining the steadiness of CLOBs.